Football built this empire

LSU Athletics is not a diversified sports portfolio. Football pays for everything else. To understand the financial strain on the department, start with what each sport earns and what it costs.

CNBC valued LSU Athletics at $1.05 billion in 2025—12th among all college programs nationally. A billion-dollar enterprise. It’s big business and an economic driver in Baton Rouge and across the state.

Strip out football and you have roughly $200–270 million in combined value across the remaining programs. Ten sports. Hundreds of athletes. Eight baseball national championships. A gymnastics program that just won a national title in front of three consecutive sold-out arenas. Collectively, they’re worth about a quarter of what one program generates alone.

What it means: LSU Athletics isn't a diversified sports portfolio. It's a football franchise that funds everything else. Understanding what each program is actually worth—and what it's costing—is the first step toward understanding the financial pressure building across the entire department.

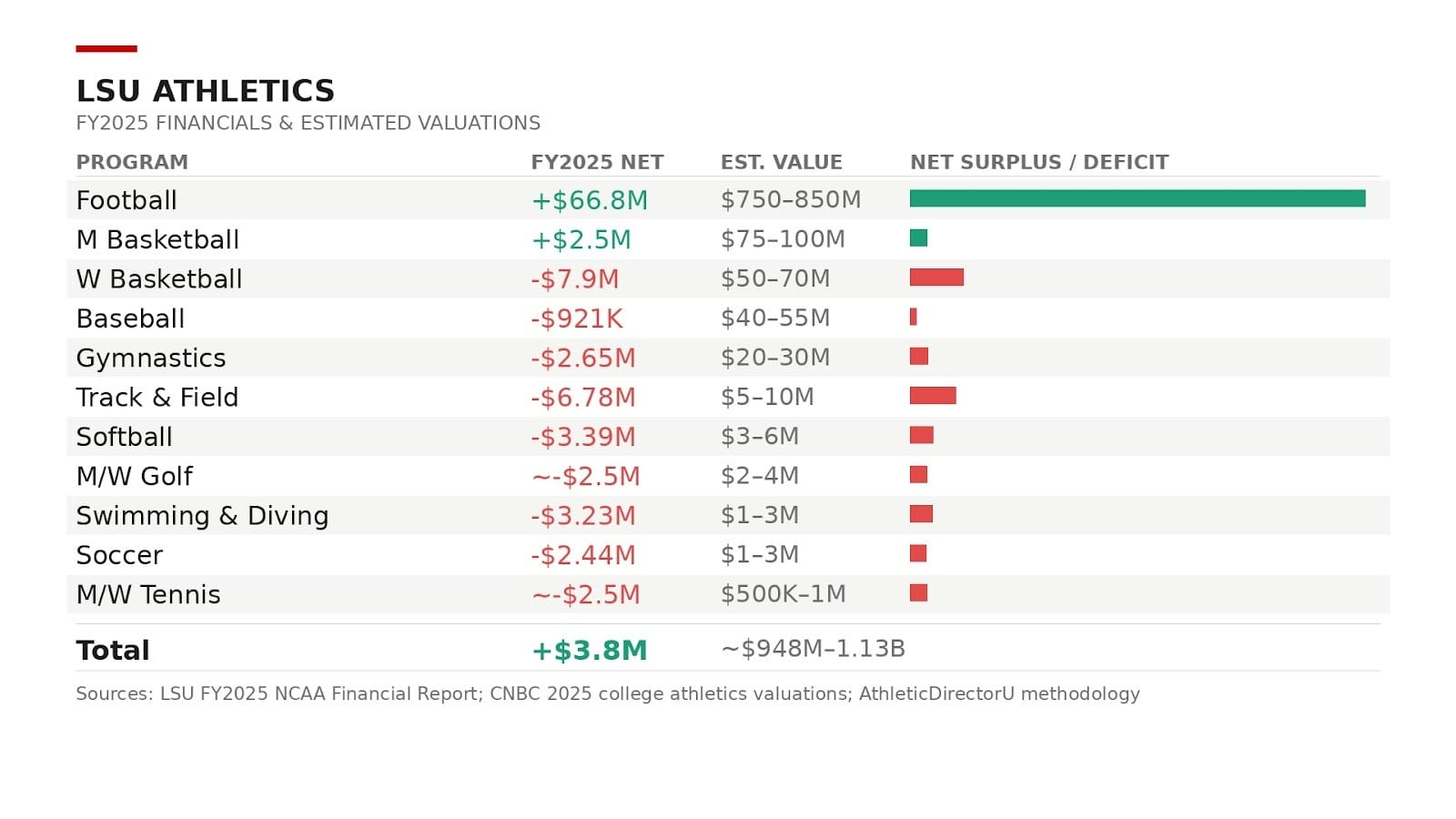

The crown jewel: Football generated $117.5 million in revenue against $50.7 million in expenses in FY2025—a record $66.8 million surplus. A 57% profit margin. It has never cleared $60 million in profit before.

Apply a 6–7x revenue multiple—justified by the SEC media contract, Death Valley's 102,000-seat footprint and a blue-chip NIL brand—and football's standalone value lands at an estimated $750–850 million—a near-NFL-caliber franchise with a captive regional fanbase and an SEC media deal escalating through 2034.

- It is effectively 75–80 cents of every dollar in LSU's $1.05 billion valuation.

The remaining portfolio: Everything else, except men’s basketball, runs at a loss. Some of those losses are strategic investments. Some are compliance obligations. The difference matters.

Men's basketball is the one program that can claim structural profitability—$2.5 million net in FY2025, four straight years in the black, almost entirely because of the SEC's television contract. Media rights contributed $6.8 million even in a 14–18 season. The Will Wade hire is a signal that LSU isn't satisfied with the floor.

- Estimated valuation: $75–100 million. The floor is the SEC contract. Without a tournament run, the value remains on the floor.

Women's basketball loses $7.9 million annually. Mulkey's $6 million salary structure is the primary driver. But the national brand—back-to-back Elite Eights, Flau'jae Johnson, the most visible women's program in the SEC not named South Carolina—generates media cycles no other non-football LSU program can approach. The program receives no SEC or NCAA media distributions, the single largest structural gap in the portfolio.

- Estimated valuation: $50–70 million. In five years, potentially double.

Baseball is the regional soul of the program. Eight national championships. A $10 million revenue base built almost entirely on tickets and contributions. A $921K deficit in the year it won the national title. Alex Box Stadium is a civic institution.

- Estimated valuation: $40–55 million—comparable to a Triple-A franchise with significantly better brand equity. The College World Series is the revenue catalyst. It isn't guaranteed annually.

Gymnastics is the department's most compelling paradox. The 2024 national champions finished first nationally in attendance with three consecutive sold-out PMAC crowds—and generated under $700,000 in direct revenue against a $3.3 million cost base. The Olivia Dunne NIL era made LSU gymnastics a national media property well beyond the sport's traditional audience. Dunne's graduation, along with nine other seniors, creates real near-term brand risk.

- Estimated valuation: $20–30 million—almost entirely optionality, if the monetization thesis holds. Less if it doesn't.

Track and field owns the most championship hardware on campus—women's outdoor alone has 14 national titles, women's indoor 11—and generates almost no commercial revenue. Institutional prestige. Olympic pipeline. Minimal commercial value.

- Estimated valuation: $5–10 million.

The compliance tier—softball, swimming, soccer, golf and tennis—collectively loses roughly $14–15 million annually. Softball has the most legitimate long-term upside as ESPN's investment in women's sports accelerates. The rest are nominal assets at best.

- Estimated valuation: $8–17 million combined.

The full picture:

The bottom line: LSU Athletics is a billion-dollar holding company with one crown jewel and a portfolio of brand investments, civic obligations and compliance programs.

Editor's note: Program valuations are estimates based on a standard revenue multiple methodology used by CNBC, Sportico and AthleticDirectorU to value college athletic programs. Individual sport valuations apply a 4–7x revenue multiple adjusted for conference affiliation, brand strength, NIL ecosystem, media rights access and profit/loss trajectory. Financial data sourced from LSU's FY2025 NCAA financial report. Valuations reflect open-market estimates only and do not represent actual transaction values.